The 2017 Tax Cuts and Jobs Act (H.R. 1) was approved by Congress and signed into law by President Trump on December 22, 2017. This historic tax bill impacts every individual and business filer, as the bill includes major changes in tax rates, deductions, and credits. What are the key changes for individuals to be cognizant of?

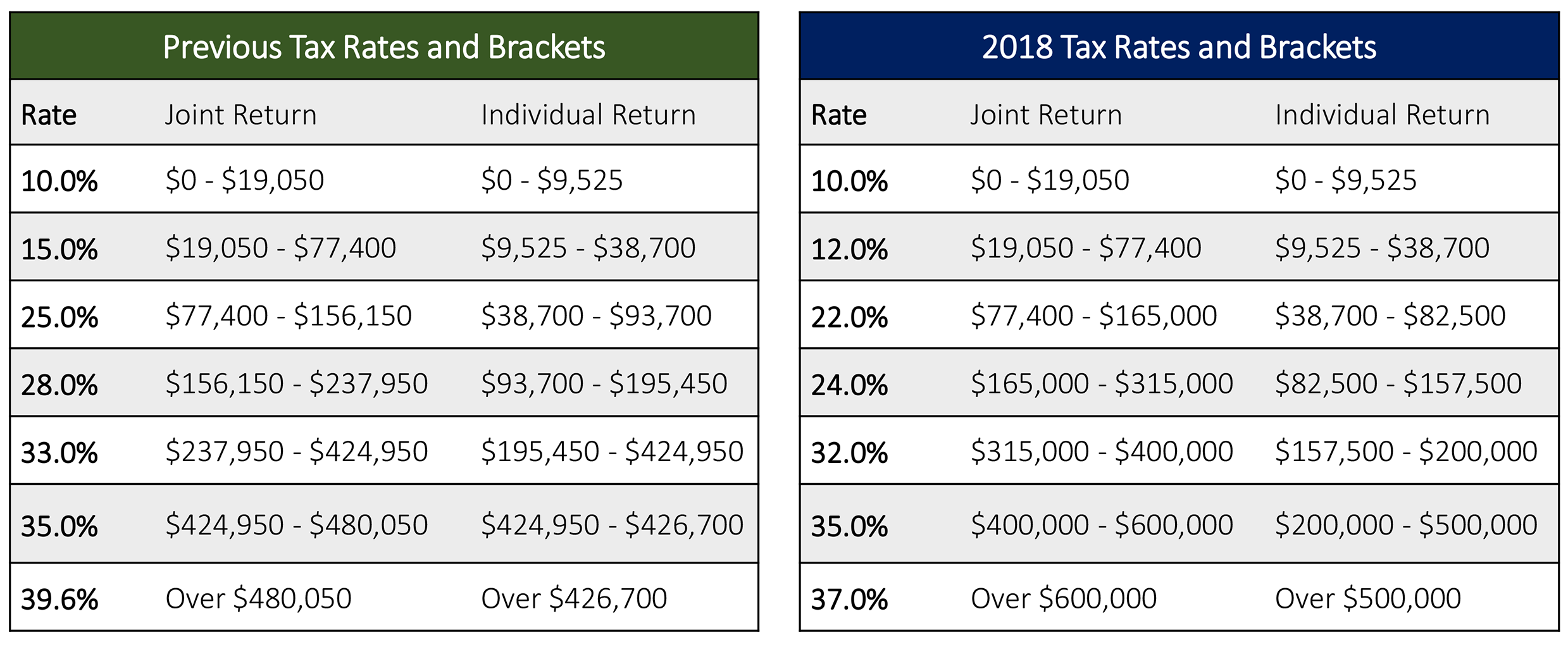

1. Tax Rates

The individual tax rates in the new law are effective starting in 2018 through 2025. The tax rates and brackets are itemized in the table below with the new rates and corresponding brackets shown on the right, in comparison to the previous law’s tax rates and corresponding brackets on the left.

2. Standard Deduction

Provisions of H.R. 1 affecting all individuals includes the elimination of the deduction for personal exemptions and the near doubling of the standard deduction. The major goal of the tax reform is to simplify filing; the higher standard deduction that replaces the personal exemption will cut more than half the number of taxpayers who have previously been itemizing deductions.

3. Itemized Deductions

Annual itemized deductions for all state and local taxes, including property taxes, is now capped at $10,000. Sales tax may be included as an alternative to claiming state and local income taxes.

There are new limits of mortgage debt for purpose of the mortgage interest deduction. The new law limits the mortgage interest deduction to interest on $750,000 of acquisition indebtedness; $375,000 for married taxpayers filing separately. This applies to tax years beginning after December 31, 2017 and beginning before January 1, 2026, for acquisition indebtedness incurred after December 15, 2017. Acquisition indebtedness incurred before December 15, 2017 is grandfathered into the previous debt limits of $1,000,000 married filing joint and $500,000 for married taxpayers filing separately.

The new law also temporarily repeals all miscellaneous itemized deductions that were previously subject to the two-percent floor, through December 31, 2025. Casualty losses will only be allowed for losses in federally declared disaster areas.

4. Family & Child Tax Credit

An enhanced child and family tax credit will also benefit many families and help to offset the loss of personal exemptions. Under H.R. 1, the child tax credit is increased from $1,000 to $2,000 per qualifying child. Up to $1,400 of that amount would be refundable. It also raises the adjusted gross income phaseout thresholds, starting at adjusted gross income of $400,000 for joint filers ($200,000 for all others). Furthermore, the child tax credit is modified to provide for a $500 nonrefundable credit for qualifying dependents other than qualifying children.

5. Alternative Minimum Tax: Exemption Amount and Phaseout Thresholds

H.R. 1 temporarily increases the alternative minimum tax (AMT) exemption amounts for individuals, for the 2018 through 2025 tax year. The AMT generally imposes a minimum tax on taxpayers who have substantially lowered their regular tax liability by taking advantage of tax-favored and preference items, including deductions, exemptions, and credits. Beginning in tax year 2018, the AMT exemption amounts are:

- $109,400 for married individuals filing jointly or surviving spouses;

- $70,300 for single or head of household filers; and

- $54,700 for married individuals filing separately (i.e. 50 percent of the amount for married individuals filing jointly).

The new law also raised the AMT exemption phaseout levels so that the AMT will apply to an income level of $1 million for married individuals filing jointly or surviving spouses, and half this amount for all other individuals. The reduction in deductibility of state and local taxes, sales tax and property taxes will also dramatically reduce the number of people subject to the AMT.

6. Education

H.R. 1 modifies qualified tuition programs (529 plans) permanently and temporarily allows for the discharge of student loan debt due to death or total and permanent disability to be excluded from income for the 2018 through 2025 tax year. Section 529 plans have, in recent years, become a popular way for parents and other family members to save for a child’s college education. Beginning after December 31, 2017, 529 plan participants may withdraw up to $10,000 per student in expenses for tuition in connection with the enrollment or attendance of the designated beneficiary at a public, private or religious elementary or secondary school.

7. Alimony

For divorces or separation instruments executed after December 31, 2018, H.R. 1 repeals the deduction for alimony payments and their inclusion in the income of the recipient.

8. Federal Estate Tax

H.R. 1 doubles the basic exclusion amount for federal estate and gift taxes and the exemption amount for the generation-skipping transfer (GST) tax. For the estates of decedents dying and gifts made after 2017 and before 2026, the amount increases from $5.6 million to $11.2 million for 2018. These figures are adjusted for inflation each year.

9. Affordable Care Act

H.R. 1 reduces the amount of the individual shared responsibility payment, making the penalty zero for tax years beginning January 1, 2019. The individual mandate penalty remains in effect for the 2018 tax year.

As always it is important to maintain a comprehensive tax plan, in order to anticipate the implementation, subsequent expiration, and potentially extension of the changes put forth by the Tax Cuts and Jobs Act. Should you have any questions regarding the changes highlighted here, be sure to contact us.